Welcome to the next installment of our Evidence-Based Investment Insights: Group Intelligence and the Market.

When it comes to investing (or anything in life worth doing well) it helps to know what you’re facing. In this case, that’s “the market.” How do you achieve every investor’s dream of buying low and selling high in a crowd of highly resourceful and competitive players? The answer is to play with rather than against the crowd, by understanding how market pricing occurs.

The Market: A Working Definition

Technically, “the market” is a plural, not a singular place. There are markets for trading stocks, bonds, commodities, real estate and more. You can think of these markets as a single place, where opposing players are competing against one another to buy low and sell high.

Granted, this “single place” is huge, representing an enormous crowd of participants who are individually and collectively helping to set fair prices every day. That’s where things get interesting

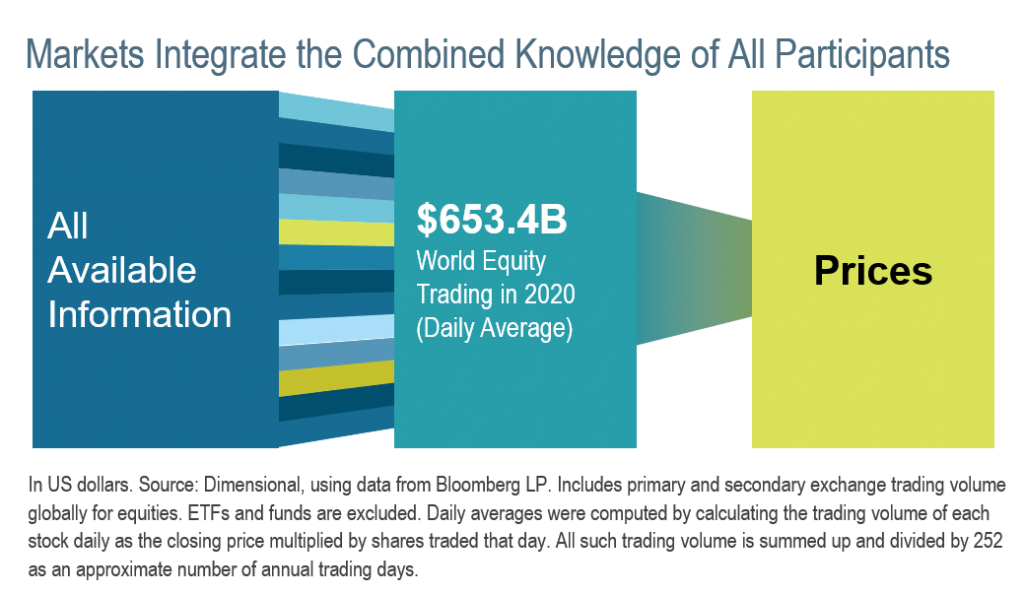

The market effectively enables competition among many market participants who voluntarily agree to transact. This trading aggregates a vast amount of information to determine security prices.

Group Intelligence: "We" Know More

Before the academic evidence showed us otherwise, it was commonly assumed that the best way to make money in what seemed like an ungoverned market was by outwitting others at forecasting future prices and trading accordingly.

Unfortunately for those who are still trying to operate by this outdated strategy, a simple jar of jelly beans illustrates why it’s an inherently flawed approach. Research has revealed that the market is not so ungoverned after all. Yes, it’s chaotic, messy, and unpredictable when viewed up close. But it’s also subject to a number of important forces over the long run.

One of these forces is group intelligence. The term refers to the notion that, at least on questions of fact, groups are better at consistently arriving at accurate answers than even the smartest individuals in that same group … with a caveat: each participant must be free to think independently, as is the case in our free markets. (Otherwise peer pressure can taint the results.)

The Jelly Bean Jar

In his landmark book “The Wisdom of Crowds,” James Surowiecki presented and popularized an enormous body of academic insights on group intelligence.

Take a large jar of jelly beans, for example. In one experiment, 56 students guessed how many jelly beans were in a jar that held 850 beans. The group’s guess – i.e., the aggregated average of the students’ individual guesses – came relatively close at 871. Only one student in the class did better than that. Similarly, structured experiments have been repeated under various conditions; time and again the group consensus was among the most reliable counts.

Participants were asked to estimate the number of jelly beans in a jar.

Range: 409-5,365

Average: 1,653

Actual: 1,670

Now apply group wisdom to the market’s multitude of daily trades. Each trade may be spot on or wildly off from a “fair” price, but the aggregate average incorporates all known information contributed by the intelligent, the ignorant, the lucky, and the lackluster. Thus the current prices set by the market are expected to yield the closest estimate for guiding one’s next trades. It’s not perfect mind you. But it’s assumed to represent the most reliable estimate in an imperfect world.

Your Takeaway

Understanding group intelligence and how it governs efficient market pricing is a first step in more consistently buying low and selling high in free capital markets. Instead of believing the discredited notion that you can regularly outguess the market’s collective wisdom, you are better off concluding that the overall market is best at forecasting prices. Your job then becomes efficiently capturing the returns that are being delivered.

Next up, we’ll explore what causes prices to change. Chances are, it’s not what you think.